Introduction

AI momentum is sweeping insurance, and the industry’s biggest cost center — claims — is squarely in the crosshairs. Insurers have always faced tension between customer experience and financial security when it comes to paying claims. It’s a crucial point in the insurer-insured relationship: Dissatisfaction with the claims process is fairly likely to cause a customer to shop for a new carrier.

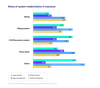

In a Celent survey of auto claimants, 12% of non-catastrophe (CAT) claimants and 6% of CAT claimants were somewhat or extremely dissatisfied with their claim process. From there, 4% of non-CAT claimants and 3% of CAT claimants had already or were actively looking to switch insurers. Some more back-of-the-envelope math shows that a third of non-CAT claimants — and half of CAT claimants — who have a bad experience change insurers. That means for every four customers who have a bad claims experience, one or two will leave.

Granted, another way to view those relatively low percentages is insurance companies are doing a pretty good job with claims, with only one in 10 or more claimants overall expressing any amount of dissatisfaction. But personal auto claims are some of the lowest paying in the insurance industry.

According to the Insurance Information Institute (III), about 4.5% of auto insurance customers had a collision claim in 2023, with an average cost of $5,521. (This is the highest claims frequency for auto, eclipsing any liability or comprehensive claims.) That same year, 5.3% of homeowners had a claim of any kind — to the tune of more than $20,000 on average. While bodily injury liability claims in auto can cost that much, that accounts for less than 1% of policyholders each year.

To recap: The most common type of auto claims costs a quarter of what the average home insurance claim costs — and with more outlays, more tension is created. Lower-cost claims are more likely to be straight-through processed, because there’s less material to work with for leakage. Considering most auto claims fall under this category, it’s a safe bet that the claims we surveyed on were handled in a relatively breezy manner.

How AI can assist in complex claims

In the insurance industry, it’s said that the most complex claims — which account for anywhere from 5% to 15% of the total — can account for up to 85% of claims costs. This is the biggest leverage point for insurers on the claims side as they look to normalize costs. Years of raising rates to account for post-pandemic inflation have tapped out the average policyholder. In order to achieve cost containment, insurers need to look internally, and they need to look at their complex claims that represent the largest pool of money from which to draw on.

There are several ways that AI can assist in reducing the outlays to complex claims:

More efficient processing: If adjusters are able to move claims along faster and easier, there’s less loss adjusting expenses incurred.

Better fraud, subrogation and salvage detection: With a closer AI view of the data as it’s coming into the claim, opportunities to claw back costs can emerge.

Litigation prevention: There’s a correlation between cycle times and propensity for a claim to go to expensive litigation. Speedier processing creates satisfied customers who don’t go to court.

Claims modernization has already been a relatively high priority for insurance companies over the past few years. Celent’s latest Dimensions survey of North American insurers finds that claims is the third-most likely carrier system to be on a modern platform and the most likely to be with a modern vendor solution.

That’s good news for claims leaders, because leveraging AI in the claims value chain is going to require a modernized base of technology to build on. Achieving the kinds of quick wins required to get results from a cycle time perspective today is more easily accomplished by leveraging point solutions — either homegrown or via a vendor — which require a modern, API- and microservices-driven architecture to spin up.

> Learn more | Expert insights on how insurers are advancing AI agent adoption

LLMs and agentic AI are industry game-changers

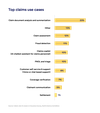

When it comes to use cases, Celent research has found that most insurers are using AI to assist claims workers with managing and parsing the many verbose documents that are part and parcel to the adjusting workflow. Ingestion capabilities leveraging early AI such as optical character recognition (OCR) and machine learning, along with RPA, have had mixed results. Some data that appears structured to the human eye doesn’t to these technologies.

But the advent of large language models (LLMs) and agentic AI frameworks is a game-changer for the industry. These technologies offer advanced capabilities for document ingestion, allowing for semi-autonomous processing of documents in many formats and via several intake channels. This presents both opportunities and challenges for insurance carriers, who must strategically decide how to integrate these technologies into their digitalization roadmaps.

As gen AI and agentic AI is leveraged more across the wider economy, customers and employees alike will develop new standards for digital capabilities. For traditional documents with any sort of structure — such as those issued by governments, medical facilities or other institutions like police reports, medical bills or repair estimates — it will soon be table stakes to extract the mission-critical data contained within them with limited friction.

They also will expect insurers to be able to ingest data and documents however they are able to get them to the carrier, whether through portal uploads, email attachments or even text messages, whether they are converted to a PDF or contained in a snapshot. And they’ll expect to be able to send a range of unstructured data — like photos, audio recordings or even social media posts — especially at the time of claim, when information is coming to the insured rapidly and they want to get their claim over the finish line as soon as possible by adding as much information as they can.

With the insurance industry informally choosing document analysis and summarization as a starting point for integrating AI with claims — and deployments proliferating across P&C — insurers should start thinking today about what’s next. It’s Celent’s belief that the claims copilot, which integrates the yes-or-no queries about what’s in a document with next-best-action and other decisioning support, could be revolutionary to the claims adjusting workflow.

It starts with automation

With the simplest claims automated to a large degree, entry-level claims personnel will likely be working more often on complex claims right off the bat to gain valuable workplace knowledge. Adding training time for less-experienced adjusters to complex claims might seem at cross purposes with the goal of reducing the cycle time on those claims in order to reduce the expenses associated with them. But that’s where the AI agents come in.

A natural language interface that is trained on the plethora of claims-related documentation and supplemented by smart workflow coding can shorten the route adjusters take from novice to expert as they work on the more complex and more expensive claims. There’s also a practical component to preparing to build agentic AI capability into the claims administration workflow: As AI continues to be consumerized, new talent entering the workplace will be used to working with prompts, not menu-diving.

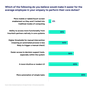

Peers across the industry already recognize this. In a late 2025 Celent survey, decision support, automation and more intuitive user interfaces were cited as the top three improvements insurers could make for their staff.

Conclusion

For carriers looking to make a difference in their employee and customer retention, continuing recent investments in claims digitalization to leverage AI is a sure-fire winner with all stakeholders.

About the author

Nathan Golia is a senior analyst in Celent’s North American property and casualty insurance practice. Before joining Celent, Nate worked as a trade journalist exclusively focused on digital transformation in the insurance industry for 13 years. As an analyst, Nate’s goal is to help insurance companies identify winning paths for acquiring and retaining policyholders by leveraging data and digital across the value chain. In addition to his brand’s conferences, Nate has spoken at a wide range of insurance events, including Insurtech Connect, IASA, AHOU and Insurtech Hartford. He also has moderated and appeared in many web seminars and other online events.

Article

A policyholder-first approach to the insurance experience

Celent analyst explores how insurers can improve the online customer experience through customer focus and digitization.

Article

Adapting to generational shifts: Meeting the changing needs of insurance agents

As the older generation retires, agents' needs — and preferences — are changing. Celent's Karlyn Carnahan explores how insurers can adapt.

Article

Success stories: How Hyland helps insurers innovate and automate

Explore how insurers have automated tedious tasks, increased their ROI and enhanced experiences with process and application intelligence solutions.

Article

Why modernization, automation and AI are key to insurance innovation

Explore key challenges, benefits and use cases for advanced technologies that can put insurers on a path to success.